June 2017

REGULATORY DEVELOPMENTS

Treasury Report on Financial Regulation

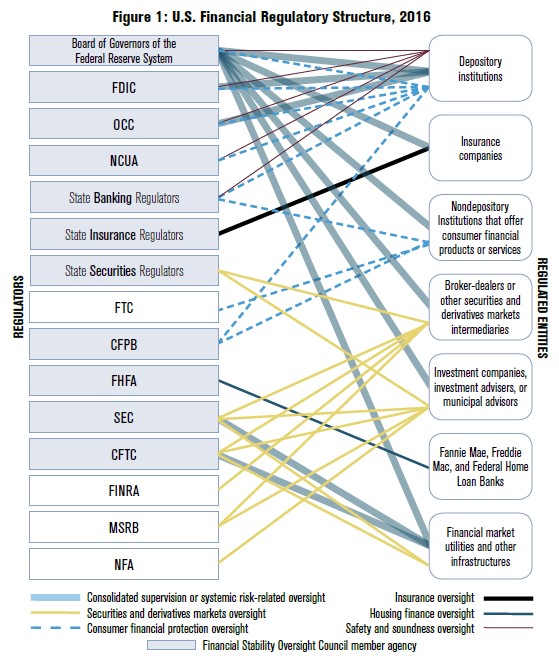

On June 12, the Treasury Department released a report, A Financial System That Creates Economic Opportunities, in response to President Trump’s executive order defining financial regulatory “Core Principles.” The Treasury report provides numerous recommendations for changes to the U.S. financial regulatory system and identifies Treasury’s view as to whether each recommendation can be implemented through regulatory action or through Congressional action.

An overarching recommendation was for Congress to take action to reduce regulatory fragmentation, overlap, and duplication. The report included the figure below, which we thought was interesting.

Other notable recommendations included:

| Recommendation | Policy Responsibility | |

|---|---|---|

| Congress | Regulator | |

| DFAST threshold: The threshold for participation for company-run DFAST should be raised to $50 billion in total assets (from the current threshold of more than $10 billion). The banking regulators should be granted authority to further calibrate this threshold on an upward basis by reference to factors related to the degree of risks and complexity of the institution. | Congress | FRB, OCC, FDIC Regulation |

| DFAST process: The mid-year DFAST cycle should be eliminated, and the number of supervisory scenarios should be reduced from three to two—the baseline and severely adverse scenario. | Congress | FRB, OCC, FDIC Regulation |

| LCR: The scope of application of the LCR should be narrowed to apply only to internationally active banks: The U.S. LCR should be limited to G-SIBs and a less stringent standard should be applied to internationally active bank holding companies that are not G-SIBs. | FRB, OCC, FDIC Regulation | |

| Creating an “off-ramp” for well-capitalized banks: Congress should consider establishing a “regulatory off-ramp” from all capital and liquidity requirements, nearly all aspects of Dodd-Frank’s enhanced prudential standards, and the Volcker Rule for depository institution holding companies and IDIs. This approach would require an institution to elect to maintain a sufficiently high level of capital, such as a 10% non-risk-weighted leverage ratio. | Congress | |

| Simplifying the capital regime: Treasury recommends keeping the standardized approaches for calculating risk-weighted assets but reducing reliance upon the advanced approaches for calculating firms’ overall risk-based capital requirements. However, U.S. regulators should consider where it would be appropriate to introduce more appropriate risk sensitivity, such as in the measurement of derivative and securities lending exposures for the standardized approaches and the proposed SCCL. | FRB, OCC, FDIC Regulation | |

| Changing liquidity requirements: There should be expanded treatment of certain qualifying instruments as HQLA. This would include categorizing high-grade municipal bonds as Level 2B liquid assets (currently they are not generally counted as HQLA). In addition, improvements should be made to the degree of conservatism in cash flow assumptions incorporated into calculations of the LCR to more fully reflect banks’ historical experience with calculation methodologies. | FRB, OCC, FDIC Regulation | |

| Volcker Rule: Exempt banking entities with $10 billion or less in assets from the Volcker Rule. | Congress | |

| Volcker Rule: Exempt banking entities with over $10 billion in assets that are not subject to the market risk capital rules from the proprietary trading prohibitions of the Volcker Rule. | Congress | |

FDIC Adopts Supervisory Guidance on Model Risk Management

On June 7, the FDIC announced that it was adopting Supervisory Guidance on Model Risk Management (FIL-22-2017) that had previously been issued by the Federal Reserve (FRB SR 11-7) and the OCC (Bulletin 2011-12). The guidance addresses supervisory expectations for model risk management, including: model development, implementation, and use; model validation; and governance, policies, and controls. The FDIC is adopting this guidance to facilitate consistent model risk-management expectations across the banking agencies and industry.

Proposed Revisions to Call Reports – No Impact on BOLI

On June 27, the banking regulators issued press releases requesting comments on proposed revisions to the Consolidated Reports of Condition and Income (Call Reports). The proposal results from ongoing efforts by the Federal Financial Institutions Examination Council (FFIEC) to ease reporting requirements and lessen the reporting burden.

The line items for BOLI in Schedules RC-F and RC-R remain unchanged.

LEGISLATIVE DEVELOPMENTS

H.R. 10 – The Financial CHOICE Act

On June 8, the House passed the Financial Choice Act of 2017 (H.R. 10). The legislation now awaits action by the Senate and there is speculation that Senate Democrats may block the legislation.

As we’ve discussed previously, the bill does not appear to have material implications for BOLI, but Section 901 would repeal the so-called Volcker Rule.

OTHER DEVELOPMENTS

Nebraska Department of Insurance Releases COLI Group Life Form Filing Requirements

On June 13, the Nebraska Department of Insurance released COLI Group Life Form Filing Requirements. The press release did not explain the action, but it appears to be an effort to clarify that group life contracts for COLI can receive discretionary group approval provided certain requirements are met.

Nebraska’s group life statutes identify a number of permissible forms of group life contracts; however, they each specify that the contract must be for the benefit of persons other than the entity to which the group life contract is issued.

The recently released filing requirements include the following statement:

Although COLI does not qualify as an eligible group under Nebraska statutes 44-1602 through 44-1606.02, a group filing may be approved if it is substantially similar to an eligible group; and it includes an explanation with a certification signed by a company officer establishing that: 1. The issuance of the group policy is not contrary to the best interests of the public. 2. The issuance of the group policy would result in economies of acquisition or administration. 3. The benefits are reasonable in relation to the premiums charged.